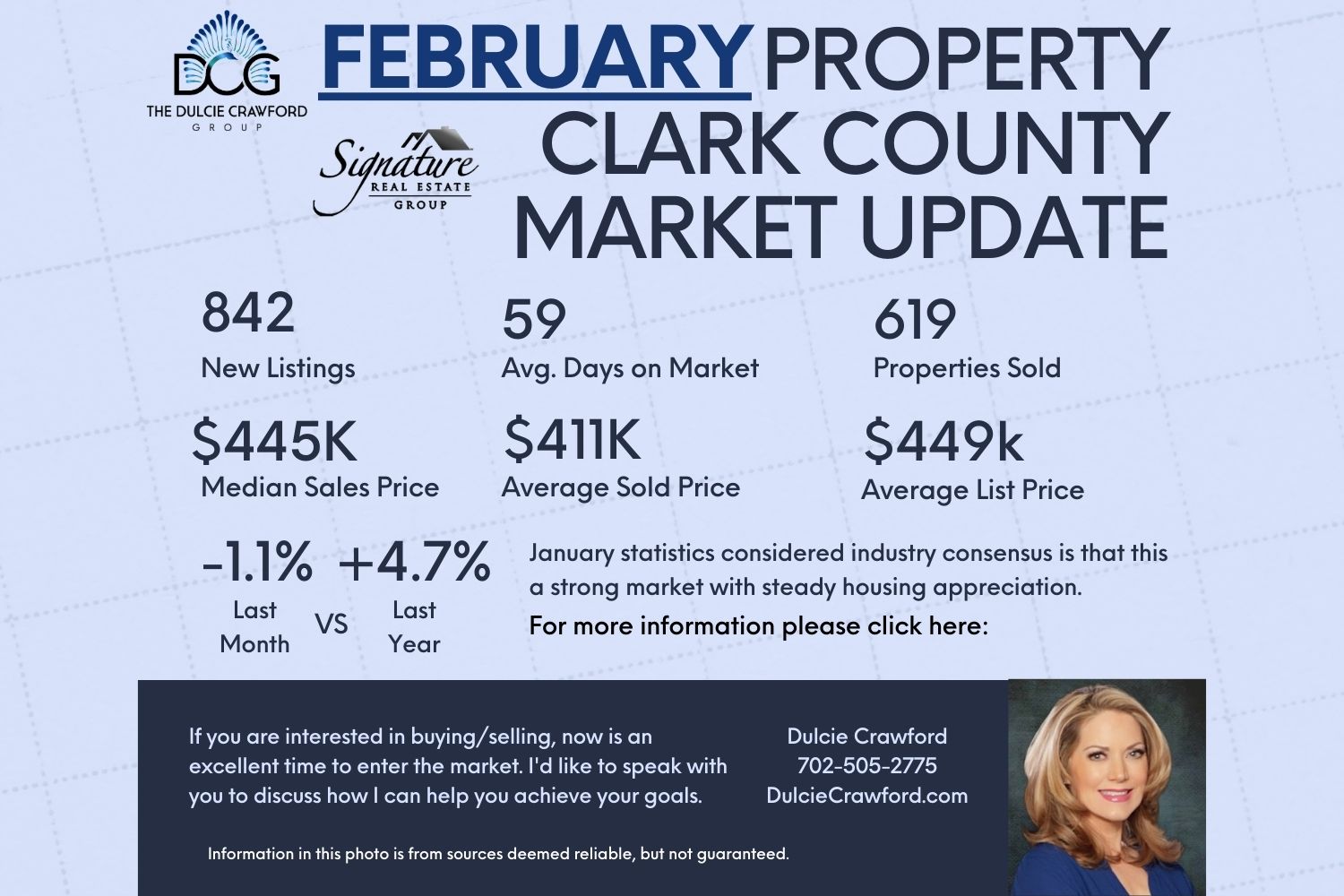

Good afternoon, our Market Watch insider specialists have quite a lot of interesting news coming from the Federal Reserve meeting in late January. Inflation is down, Wages are going up and consumer confidence is the highest it’s been in three years but the Federal reserve is steadfast in its goals to continue to battle inflation down to 2%. Of course, this means that since most people including 34% of market analysts who believed that interest rate cuts would start this summer around March will now more realistically be looking at federal interest rate cuts happening 2 months later in May at the earliest. Naturally it will likely take the Federal Reserve cutting their interest rates before we see any meaningful drops in the housing market mortgage rates. My Market Experts are predicting that they expect rates to settle in around 6.25% for second half of 2024. Waiting to buy, could be a mistake, based on the market supply to be expected to remain low, and appreciation expected to grow another possible 6% this year. Buyers sitting on the sidelines, will end up costing themselves the ability to buy at lower prices, vs buying now and refinance later when the rates drop. Many Buyers that wait too long, will possibly end up being priced out of the market altogether.

So far in 2024:

– Asking prices nationally are now 3% higher than last year.

– Price of new listings are now about 5% higher than a year ago

– Price of homes now in contract are nearly 7% higher than 2023

According to Mortgage News Daily, The National Average rates were DOWN. (Local Rates are often lower)

- 6.90 Conventional 30 yr

- 6.29 conventional 15 yr

- 6.30 conventional 5/1arm

- 7.25 jumbo 30 year

- 6.20 FHA 30 yr

- 6.20 VA 30 yr

Non-QM Rates, like bank statement loans and no doc investors loans, are about 1-2% higher.

Federal Chairman Powell had some interesting comments on housing recently and they are summarized below.

- Said their goals are maximum employment and price stability. Not just housing price stability but all prices on all things.

- Said they’re not targeting housing price increases nor the cost of housing.

- Said they’re aware that when they cut rates, at the beginning of the pandemic, the housing industry was helped more than any other industry.

- Said they know that when they raise the rates, at the beginning of the pandemic, the housing industry can be hurt because it’s a very rate sensitive industry.

- Acknowledged that we have longer term problems with housing inventory.

More and more home investors are coming off the sidelines. The yearly rate of core inflation slowed to 2.9%, the lowest level in almost three years. Keep in mind, the Federal reserve has said they want it at 2% and that is not far off and lower rates are likely coming later this year. Home prices are also up 5% from a year ago and UP almost 50% since just prior to the pandemic. The drop-in mortgage rates since October means the average buyer is paying $200 less per month for their mortgage or can afford $40,000 in more home price. In general, a homebuyer with a $3,000 Monthly housing budget can now afford a $453,000 home.